Realty Perspective – June 2024

0800 424 368

027 443 5538

Welcome to our Sunflower Growing Competition page. Here you will find everything you need to...

Continue reading

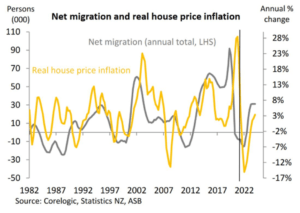

2025 vs 2024 - Same Same, But Different The last year brought more certainty and stability to...

Continue reading

Reflecting on a Year of Stability in 2024 After navigating the challenges of...

Continue reading